In a bold move, Deutsche Bank, Germany’s largest financial institution with a $54 billion market cap, is reportedly exploring the launch of a euro-pegged stablecoin. This signals a great shift in the digital asset landscape.

This strategic pivot is part of the bank’s Project Dama 2. This project aims to enhance cross-border payments and compete in the tokenised asset market. To survive in the competitive stablecoin market, the project could potentially leverage Ethereum or a hybrid blockchain like Solana.

Consequently, this initiative positions Deutsche Bank as a formidable player in the rapidly evolving stablecoin ecosystem. This move challenges both traditional financial institutions and established cryptocurrency issuers.

Furthermore, it raises critical questions about the role of stablecoins in modern finance. Moreover, it sheds light on stablecoin’s competition with central bank digital currencies (CBDCs) and their potential to redefine global transactions.

In this article, CryptoGuide GH delves into Deutsche Bank’s ambitious stablecoin push and its far-reaching implications for the market.

Deutsche Bank’s Strategic Leap into Stablecoins

Deutsche Bank’s exploration of a euro-backed stablecoin, potentially in collaboration with partners like DWS, Flow Traders, and Galaxy, accentuates its commitment to embracing digital innovation.

By integrating blockchain technology, the bank aims to streamline cross-border payments. With this, it aims to reduce transaction costs and enhance liquidity.

Unlike volatile cryptocurrencies such as Bitcoin (BTC), stablecoins maintain price stability by pegging their value to assets like the euro (€) or U.S. dollar ($). This makes them ideal for payments, remittances, and decentralised finance (DeFi) applications.

Deutsche Bank’s strategic shift reflects a growing wave of traditional financial institutions adopting digital assets to stay relevant in a rapidly evolving landscape.

With global stablecoin circulation exceeding $254 billion, led predominantly by Tether (USDT) and USD Coin (USDC) commanding the lion’s share of the market, the bank’s bold move has the potential to shake up the established order.

Additionally, by developing tokenised deposits and potentially issuing its stablecoins under the German Federal Financial Supervisory Authority (BaFin), the agency that oversees the country’s regulation, Deutsche Bank seeks to offer a secure, regulated alternative to existing stablecoins.

This strategic initiative not only enhances the bank’s digital footprint. It also positions the bank to capture a share of the projected $3.7 trillion stablecoin market by 2030.

Deutsche Bank’s Competition with Santander Bank

Meanwhile, Santander Bank has been a pioneer in integrating blockchain technology. Notably, it collaborated with the European Investment Bank (EIB) in 2021 to launch a €100 million bond on the public Ethereum network.

This move demonstrated Santander’s commitment to leveraging digital assets for capital market innovation. John Whelan, Managing Director of Digital Assets at Santander CIB, emphasised the growing client interest in stablecoins for faster cross-border payments and automated treasury operations.

However, Deutsche Bank’s stablecoin push could intensify competition with Santander. While Santander focuses on blockchain-based securities and client-driven digital asset solutions, Deutsche Bank’s potential euro-pegged stablecoin targets a broader scope. This includes tokenised deposits and cross-border payment optimisation.

Furthermore, Deutsche Bank’s joint venture with industry players like Galaxy and Flow Traders suggests a collaborative approach. This could potentially give it an edge in scalability and regulatory compliance.

In contrast, Santander’s strength lies in its early adoption of blockchain for bond issuance and its established client base. Despite its $54 billion market cap, Deutsche Bank’s venture into a tailored Layer 2 blockchain with ZKsync technology signals a great push for enhanced adaptability and innovation in the digital asset space.

Consequently, the rivalry between these banking giants will likely drive innovation. This could force Santander and Deutsche Bank to refine their offerings to attract corporate and retail clients seeking efficient, low-cost digital payment solutions.

![]()

Deutsche Bank Competition with Mainstream Stablecoin Issuers: Circle, Tether, and PayPal

Deutsche Bank’s foray into the stablecoin arena positions it in direct competition with major players such as Tether, Circle, and PayPal. In the long term, this could intensify the battle for market dominance.

Tether (USDT), with a market capitalisation of $155 billion as of this publication, dominates the stablecoin sector. USDT accounts for more than 60% of trading volumes on crypto platforms.

However, Tether has faced scrutiny over its reserve transparency. This included a $41 million fine by the Commodities Futures Trading Commission (CFTC) in 2021 for misleading claims about its dollar backing. This regulatory baggage presents an opportunity for Deutsche Bank to offer a more transparent, bank-backed alternative.

Circle’s USD Coin (USDC), with a $60 billion market cap, is another major competitor. Known for its rigorous reserve audits and partnerships with traditional institutions like BNY Mellon, Circle’s integration with platforms like Coinbase and its focus on Web3 development make it a formidable player.

Yet, Deutsche Bank’s regulated status and potential to leverage its vast financial infrastructure could appeal to clients prioritising security over decentralisation.

PayPal’s USD-backed stablecoin (PYUSD), launched in 2023, has grown to a $1 billion market cap. PayPal has been able to achieve billion-dollar status due to its massive user base driving adoption.

Unlike Tether and Circle, PayPal benefits from its established non-crypto audience, which enables the cross-selling of financial products.

However, Deutsche Bank’s euro-pegged stablecoin could carve a niche in Europe. This is because regulatory frameworks like the European Union (EU)’s Markets in Crypto-Assets (MiCA) regulation favour bank-issued stablecoins.

Ultimately, Deutsche Bank’s ability to compete will hinge on its capacity to deliver low-cost, scalable, and compliant solutions.

Are Stablecoins Traditional Banks’ Answer to Cryptocurrencies?

Stablecoins represent a bridge between traditional finance and cryptocurrencies. The asset class offers the stability of fiat currencies with the efficiency of blockchain technology.

For traditional banks like Deutsche Bank, stablecoins provide a strategic tool to counter the volatility of cryptocurrencies like Bitcoin and Ethereum, which are unsuitable for daily transactions due to price fluctuations.

By issuing stablecoins, banks can facilitate faster, cheaper cross-border payments. This reduces reliance on legacy systems like the Society for Worldwide Interbank Financial Telecommunications (SWIFT), which often incur high fees and delays.

Moreover, stablecoins enable banks to tap into the growing DeFi ecosystem, where they serve as liquidity providers for decentralised exchanges (DEXs) and lending protocols.

Deutsche Bank’s potential stablecoin could attract tech-savvy clients, including Gen Z and businesses engaged in international trade, by offering instant settlements and programmable money.

Additionally, banks can maintain regulatory oversight, addressing concerns about money laundering and fraud that plague some crypto markets.

Thus, stablecoins empower traditional banks to modernise their services while preserving their role as trusted financial intermediaries.

Are Stablecoins Better Than Central Bank Digital Currencies?

The debate over stablecoins versus CBDCs centres around their respective strengths and limitations. Stablecoins, issued by private entities or banks, offer flexibility, interoperability, and rapid adoption.

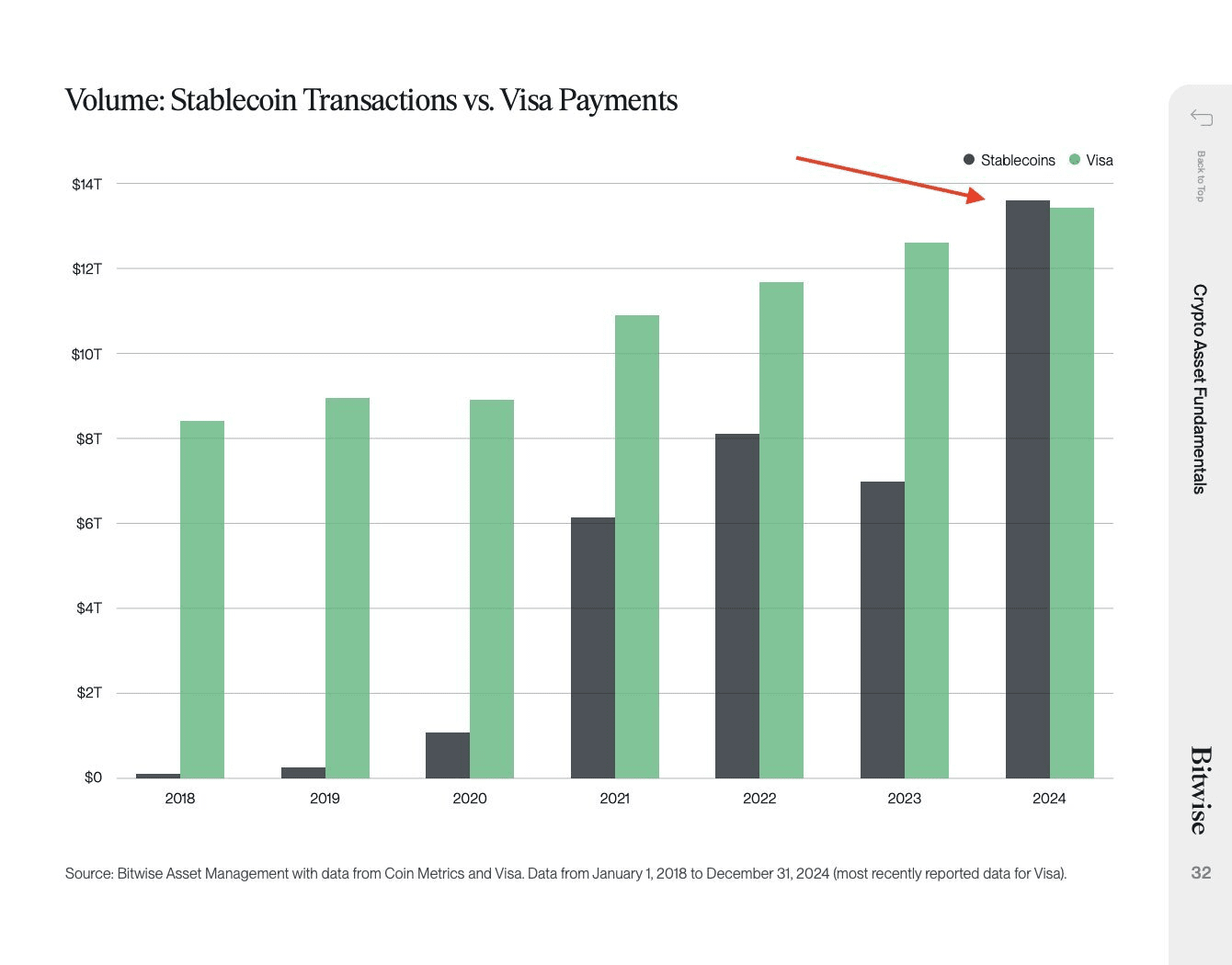

For instance, stablecoins facilitated about $14 trillion in transactions in 2024. This was a trillion dollars more than transactions processed by a financial giant like Visa. Stablecoin’s decentralised nature allows for 24/7 transactions and lower fees, particularly in emerging markets where remittance costs have dropped significantly.

In contrast, CBDCs, issued by central banks, prioritise financial stability and regulatory control. The European Central Bank’s digital euro, for example, aims to enhance monetary policy and financial inclusion but faces challenges in cross-border interoperability and adoption.

Moreover, CBDCs raise privacy concerns due to their traceability, potentially deterring users who value anonymity.

However, stablecoins are not without risks. The 2023 Silicon Valley Bank crisis exposed vulnerabilities in stablecoin reserves, as USDC depegged when $3.3 billion of its reserves were trapped.

Additionally, regulatory uncertainty persists, with stablecoins subject to oversight from multiple agencies. CBDCs, backed by central banks, offer greater trust and stability but may lack the innovation and speed of private stablecoins.

Ultimately, Deutsche Bank’s stablecoin could combine the best of both worlds: bank-backed security with blockchain efficiency.

Conclusion: Is 2025 the Year for Stablecoin Experiments?

Deutsche Bank’s foray into stablecoins marks a pivotal moment for the financial industry in 2025. By challenging competitors like Santander, Tether, Circle, and PayPal, the bank is poised to redefine the stablecoin market.

Its regulated, euro-pegged stablecoin could enhance cross-border payments, attract new clients, and strengthen Europe’s digital asset ecosystem.

Furthermore, stablecoins offer traditional banks a powerful tool to compete with cryptocurrencies while addressing the limitations of CBDCs.

Stablecoin market to hit $3.7T by 2030; Deutsche Bank’s push drives innovation, competition, adoption, reshaping global finance.